Providing financial resources and information on the microfinance industry to investors, borrowers, and professionals.

The for-profit, commercial microfinance institutions tend to only offer financial services. Sometimes an individual only needs a loan, but those who can properly manage and benefit from a high interest microloan are typically already living above the poverty line. The borrower utilizes their loan to invest in their small business. They purchase land and supplies needed to continue their already profitable business. Since it's a strictly profit based industry, the borrower's best interests are not necessarily a top priority. For example, countries, like Mexico and South Africa, that can legally authorize microloans with alarmingly high interest rates (think 60% to 100%) lead to more cases of default on loans. Investing with a commercial microfinancier, your money could go into such a market with high interest loans. As you can imagine, these loans with higher rates aren't as successful as those with lower rates.

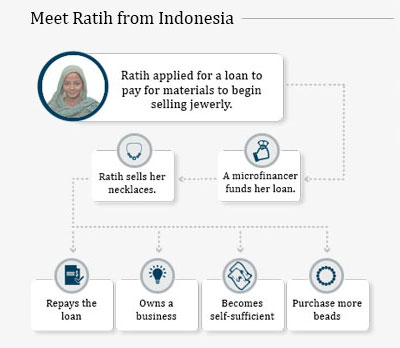

As of 2005, the oldest of the non-profit microfinanciers, Grameen Bank in Bangladesh, had lent $4 billion in microloans to 7 million borrowers in just a decade. Microcredit organizations that are non-profits, owned by investors or customers, are more focused on the economic development of the underprivileged than they are with seeking profit. Not only do these microcredit non-profits offer their customers more than just microloans, they also provide healthcare, training, and education. When the MFIs are more concerned with providing their clients these financial services for economic and social development, the microloan model can prove to be more successful in lifting the poor out of poverty. However, they extend credit at lower rates than the commercial sector. These MFIs financing the poor's businesses or expenses with affordable rates experience low default, but the cost of servicing the loans (and providing ancillary services) can be high. Much focus has shifted to being able to provide financial services online or via phone, to reduce some of these cost (and travel) burdens on both borrowers and institutions. These technologies are still developing and have unique limitations.

According to Consultative Group to Assist the Poor, microloans average a return of 5.8%. This includes small business loans, as well as consumer short term financing, and personal healthcare related financing such as access to loans for medical care or access to finance dental services.

According to World Bank, poverty in Bangladesh has reduced by 26% during 2000 to 2010. Is this decrease thanks to the microloan industry? A rise in labor income and poverty reducing programs for youth and women including early education, health, nutrition, and work skills have been the dominating factors in Bangladesh's economic turnaround. Microloans have played a part in that, as has government investment in education and industry, which has provided the greatest economic boost. Access to financial services, particularly banking, which provides the ability both to save or to borrow funds, seems to be positively correlated with development.

In the United States, we see the same trends playing a role in several niche sectors such as medical financing and wedding loans. Positive economic impact provided via microfinance also works in developed countries.